GLIMS Journal of Management Review and Transformation

Search

Search

Amareshwar Kumar Rai1 and Sanjay Srivas1

1 Software Technology Parks of India, under MeitY, Government of India, Pune, Maharashtra, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Global capability centres (GCCs) are playing a significant role in positioning India as a strategic hub in the global business landscape. This study explores the sustainability and growth of GCCs in India and their transformative impact on the Indian business ecosystem. Currently, around 1,800 GCCs operate across multiple domains and locations nationwide. Key drivers for GCCs’ establishment are the availability of skilled talent, technological advancements and policy and infrastructure support. It is important to know that GCCs are evolving from cost-arbitrage back-office hubs to centres of innovation, leadership development and strategic decision-making, and are further expected to emerge as AI-driven enterprises. In this article, quantitative analyses were performed to examine how factors such as technological advancements, workforce upskilling, and policy support contribute to fostering GCC sustainability. The study shows that significant opportunities exist to expand GCCs into Tier II and Tier III cities and diversify into emerging sectors such as telecom, real estate and healthcare. Based on the data available in terms of the state policy framework, talent pool and other conducive key factors for the establishment of GCC, some recommendations and suggestions are proposed to ensure long-term growth of the country. In conclusion, GCCs currently contribute 1.5%–2.0% to India’s GDP and employ approximately 1.9 million people and are expected to grow 3.5% GDP contribution with 2.8 million jobs by 2030, which showcases increasing economic significance. This indicates the significance of GCCs in the Indian business ecosystem.

Global capability centre (GCC), sustainable development, R&D, knowledge economy, GCC policy, leadership

Introduction

Global capability centres (GCCs), formerly known as captive centres of multinational companies, have evolved over the years into global in-house centres (GICs) and are now more commonly known as GCCs. These centres were established as cost-arbitrage hubs in the late 1990s and now emerged as strategic units within multinational corporations (MNCs) to manage key business functions across the regions. For example, Texas Instruments (TI) were the first global tech company for software design, which set up its GCC operation at Bangalore, India. However, this GCC was an R&D centre and more than cost saving move. At the same time, Citibank launched Citicorp Overseas Software Ltd. (COSL) in Pune, focused on banking software, effectively becoming India’s first ‘captive’ IT services centre. Now GCCs are service centres as well as innovation centres, creating value-added services. The most common GCCs support functions such as IT services, finance, human resources and customer support, leveraging advanced technologies and a skilled workforce (Knowledge and Innovation hub) to drive operational efficiency and innovation (Six Imperatives to Scale up the Global Capability Centre Market in India, PwC, 2023). Over the years, GCCs evolved from back-office operations into strategic decision-making operations. Development phases of GCCs over the periods are given below and depicted in Figure 1.

Figure 1. Representation of GCC Development Phases.

Note: GCC = Global Capability Centre.

In this context, a few examples are explained below to understand the transformation of back-office operations to become strategic decision-making and global leadership through a case study:

Thus, GCCs are now nerve centres of innovation, leadership and global competitiveness for MNCs.

Review of Literature

To conduct this study further, an extensive literature review on GCC implementation and the policy frameworks in India was undertaken.

India Brand Equity Foundation, in its news reports, highlights that GCCs have emerged as a critical component of India’s integration into global value chains. Over the past decade, India has consolidated its position as the world’s leading destination for GCCs, hosting more than half of the global GCC footprint. According to industry and policy reports, India currently accommodates approximately 1,700–1,800 GCCs across diverse sectors, including information technology, engineering, banking and financial services, healthcare, manufacturing and telecommunications. The literature identifies key enablers for GCC growth include large skilled talent pool, cost efficiency, robust digital infrastructure and progressive policy support (IBEF, 2024).

Phadnis (2024), in her Times of India article titled ‘How GCCs are powering India’s Job Market’, explains that several studies highlight the growing economic significance of GCCs within the Indian economy. GCCs are estimated to contribute between 1.5% and 2.0% to India’s GDP while employing nearly 1.9 million professionals. As per projections, indicate that by 2030, employment generation could reach approximately 2.8 million, with a corresponding increase in GDP contribution to around 3.5%. This highlights the transition of GCCs from auxiliary service providers to core contributors to national economic growth (Phadnis, 2024).

An India Briefing article by Melissa Cyrill and Khyati Anand brings out a very interesting perspective on the structural transformation in the functional orientation of GCCs. Earlier research characterised GCCs primarily as cost-arbitrage and back-office support units; however, recent studies demonstrate a clear shift toward innovation-led functions such as research and development, AI, data analytics, cybersecurity, cloud engineering and product development. This transition reflects a strategic realignment wherein multinational enterprises increasingly leverage Indian GCCs for high-value and mission-critical activities. Also, the estimated GCC market should reach US$110 billion by 2030 (Cyrill & Anand, 2023).

In the report by PwC, India titled ‘Catalysing value creation in Indian GCCs’, research reveals that from a strategic management perspective, GCCs are now viewed as integral components of enterprise-wide value creation. PwC’s empirical analysis highlights that Indian GCCs are contributing to global organisations at a compounded annual growth rate exceeding 11%, particularly through digital transformation and innovation initiatives. Leadership development, decision-making autonomy and closer integration with headquarters are identified as key determinants of GCC maturity and long-term sustainability (Ojha et al., 2025).

Methodology to Measure the Impact of GCCs

This study adopts a mixed-methods research design to comprehensively assess the impact of GCCs on the Indian economy. The mixed-method approach integrates quantitative techniques to measure measurable economic outcomes with qualitative techniques to capture strategic, institutional and innovation-driven impacts that are not fully reflected through numerical indicators.

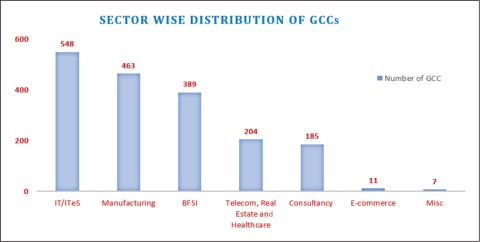

Sector-wise Distribution of GCCs

In the IT industry, it is a fact that many multinational companies have established their captive unit in India (offshore centres) to manage the entire work, such as operations, enhance innovation and drive technological advancements of the captive unit. As per the market report by JLL India, approximately 1,800 GCCs are currently operating in India in various sectors, as depicted in Figure 2. Of the total, 548 GCCs are in the IT/ITeS sector. The next three important domains for GCCs are Manufacturing, Banking Financial Services and Insurance (BFSI), Telecom, Real Estate & Healthcare which are represented by 463, 389 and 204 GCCs respectively in the said domains across the country. Further, GCC—Consultancy are known for its process-oriented and practical approach. They work closely with leadership teams with an objective to solve critical business challenges and unlock value-driven growth through the right workforce strategy, improving operational efficiency and unlocking long-term value. A few top GCCs in E-commerce, such as Amazon, Goldman Sachs, JP Morgan, Deloitte and Walmart in India, are transforming the country’s business landscape and contributing significantly to global operations.

Figure 2. Sector-wise Distribution of GCCs in India.

Note: GCC = Global Capability Centre.

Key Factors for Evolution of GCCs in India

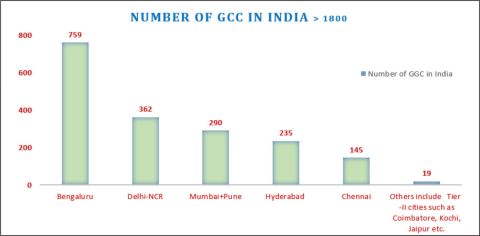

India has become a preferred destination for GCCs due to its vast talent pool, cost advantages, robust IT infrastructure and policy framework. Over the past two decades, the country has witnessed significant growth in the number of GCCs, with many global giants establishing their operations in cities like Bengaluru, Hyderabad, Mumbai, Pune, Chennai and Delhi-NCR (Ghosh, 2025). Initially, GCCs in India were primarily set up for back-office operations, focusing on repetitive and transactional tasks. However, over time, they are converted into centres of excellence, innovation hubs and strategic enablers for their parent organisations. The location-wise distribution of GCCs in India is as follows:

From Figure 3, it is clear that the preferred destination for establishing GCCs is metro cities. However, the key factors for establishing new GCCs are also available in other locations of the country (India’s Unique Value Proposition, 2025). Nowadays, many of the State Government have made GCC policies to attract their locations. For example, Uttar Pradesh, Karnataka and other states. Uttar Pradesh has issued a GCC policy 2024, which addresses the key factors that influence global companies to invest in that region (Bagri et al., 2024; GCC Policy, 2024). Gujarat has launched the GCC policy 2025–2030, aligning with union budget 2025. Now, the government is keen to expand GCCs into smaller cities by providing a conducive environment, such as robust infrastructure, improving the policy framework and strengthening the startup ecosystem required for the establishment of GCC. With regard to the startup ecosystem in Tier II locations, Next Generation Incubation Scheme (NGIS), with an objective to promote and support innovative startups, is entrusted by MeitY to STPI for implementation. The locations are Agartala, Bhilai, Bhopal, Bhubaneswar, Dehradun, Guwahati, Jaipur, Lucknow, Prayagraj, Mohali, Patna and Vijayawada. To strengthen infrastructure, STPI under MeitY has established Incubation facilities in the Tier II and Tier III locations (IBEF, 2024).

Figure 3. Location-wise GCCs in India.

Note: GCCs = Global Capability Centres.

The evolution of GCCs has been driven by:

Policy and Infrastructure: Support by the central and state-level policy frameworks:

Talent Availability: Access to a skilled and diverse workforce specialising in technology, analytics and business processes, that is:

Technological Advancements: Adoption of automation, AI and cloud computing to enhance operational capabilities. With a strong digital infrastructure, focus on emerging technologies like AI, 5G, EVs, cloud and space tech, India is continuously moving towards becoming a global technology powerhouse.

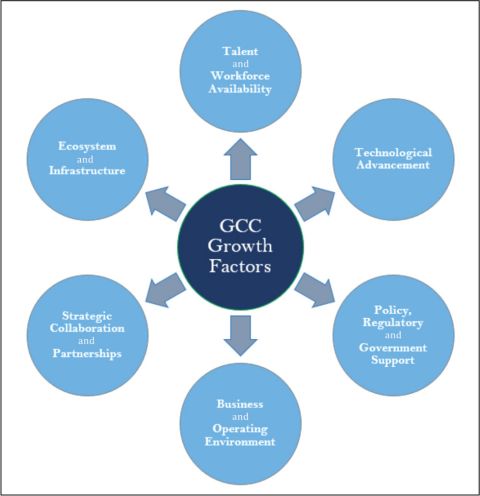

Figure 4 depicts the conceptual framework for GCC growth, showcasing the interplay among key enabling factors that collectively contribute to the maturation of GCCs in India. The framework positions talent and workforce availability, technological advancement, policy and support, business and operating environment, strategic collaboration and partnerships and infrastructure and innovation ecosystem as the core determinants of GCC growth (Jha & Seth, 2025). Each factor contributes uniquely. Together, these factors are creating a synergistic ecosystem that drives continuous evolution, resilience and strategic importance of GCCs in India.

Figure 4. Conceptual Framework for GCC Growth.

Note: GCC = Global Capability Centre.

Operational Models for Setting up GCCs

Role of GCCs in Shaping Global Business Landscape

The role of GCCs in shaping the global business landscape is multi-dimensional.

As per McKinsey’s operations report, GCCs are evolving to become multifaceted and serve many purposes.

Thus, GCCs are evolving from ‘support arms’ into strategic centres of global enterprises, shaping the business into innovation, digital transformation, decision-making and redefining the future of business.

Impact of GCCs on Indian Economics

As per industry estimates, GCCs in India generate revenue of $40–$50 billion annually and contribute 1.5%–2% of India’s GDP directly through exports and are expected to contribute roughly 3.5% of India’s GDP by 2030, generating an estimated revenue of $121 billion. According to a report by NASSCOM, the IT-BPM sector, which encompasses a substantial portion of GCCs, contributed approximately 8% to India’s GDP in the last fiscal year. On the other hand, through driving ER&D, product design and digital transformation, GCCs improve India’s knowledge economy and the inflow of foreign exchange (Reddy & Jain, 2024).

Around 1800 GCCs are operating in the country, employing over 1.9 million professionals, who are the strongest pillars of India’s knowledge economy (Jones Lang LaSalle, 2024; Times Group, 2024).

Now, GCCs are expanding from Tier 1 cities to Tier II cities such as Coimbatore, Kochi and Jaipur. These are contributing towards regional economic growth.

Recommendations and Suggestions for GCCs

As per literature, 99% of total established GCCs are established in metro cities (Tier I cities) because of the availability of required factors such as well-developed infrastructure, talent pool, industry-academia collaborations, supportive policy framework and so on, which are required for smooth and sustainable business operations. But now it is time to think about the expansion of GCCs in smaller cities, that is, Tier II cities. However, some Tier II cities such as Coimbatore, Bhubaneswar, Indore, Nagpur, Mohali/Chandigarh and Jaipur have more potential for growth of new GCCs. In order to get more expansion, the following needs to be focused on.

Conclusion

The journey of GCCs in India reflects a clear paradigm shift, beginning with cost arbitrage, progressing through process excellence, advancing toward innovation, maturing into strategic decision-making roles and ultimately transforming into AI-driven enterprises. AI-driven enterprises are a futuristic theme which will transform the global business landscape by rapid and widespread integration of AI across multiple domains. Alongside this transformation, GCCs continue to play a pivotal role in India’s growth story by creating high-quality jobs, fostering entrepreneurial mindsets and attracting substantial global investment into the Indian economy. Literature reveals that GCCs are contributing around 1.5%–2% in Indian GDP and generate substantial employment in the country. Further, increasing the number of GCCs in India and their sustainability is due to technology adoption in business operations across the Globe and policy incentives given by the Indian Government jointly.

Below is the summary of a few GCC policies launched by different states.

Karnataka GCC Policy 2024–2029

Scope: Encompasses attraction and expansion of high-value GCCs specialising in IT, AI, fintech and emerging technologies through tailored state-level incentives, positioning Karnataka as a premier GCC hub leveraging its Bengaluru ecosystem.

Targets: Aims to establish 500–1,000 new GCCs, generate 350,000 direct jobs and contribute $50 billion to the state economy by 2029, with a focus on Tier I and emerging Tier II cities.

Key incentives: Up to 100% reimbursement on rental costs for certified spaces; skilling subsidies on 50% of training expenses; funding for innovation labs and R&D facilities; expedited single-window clearances.

Value propositions: Access to India’s largest tech talent pool (Bengaluru hosts 40% of national GCCs); world-class digital infrastructure; proximity to global MNCs and startups for collaboration.

Limitations: Over-reliance on Bengaluru limits dispersal to rural areas; potential infrastructure strain from rapid scaling; competition from national policies.

Impact: As India’s first dedicated GCC policy, it catalysed 20+ new GCC commitments within six months, enhancing Karnataka’s 35% share of national GCC revenue.

Uttar Pradesh GCC Policy 2024

Scope: Targets GCC setups in tech parks and SEZs across Noida, Lucknow and Agra, emphasising electronics, IT and data analytics to diversify from traditional manufacturing.

Targets: 1,000+ GCCs and 500,000 jobs over five years, with emphasis on women-led and MSME-linked operations.

Key incentives: 100% stamp duty exemption for five years; payroll subsidies up to .png) 20,000/month per employee; land cost rebates in state IT cities.

20,000/month per employee; land cost rebates in state IT cities.

Value propositions: Cost-effective land (30%–50% cheaper than metros); young demographic with 50+ universities; improved air connectivity via Jewar Airport.

Limitations: Nascent ecosystem compared to southern states; bureaucratic delays in approvals; skill mismatches in non-metro areas.

Impact: Secured initial pledges from 10 GCCs, boosting UP’s Tier II appeal and contributing to 15% YoY GCC space uptake in 2025.

Madhya Pradesh GCC Policy 2025

Scope: Statewide promotion of mid-sized GCCs in IT, AI, fintech and BFSI, with hubs in Indore, Bhopal and Gwalior.

Targets: 50 GCCs creating 37,000 jobs by 2029, prioritising non-metro growth.

Key incentives: Capital expenditure subsidies up to 20%; payroll rebates for five years; electricity duty exemptions.

Value propositions: Lowest operational costs among top states; central logistics advantage; government-backed skilling via Atal Bihari Institutes.

Limitations: Limited international brand visibility; underdeveloped high-speed internet in interiors; smaller talent pool.

Impact: Attracted five early movers in 2025, positioning MP as a cost-arbitrage leader for back-office GCCs.

Gujarat GCC Policy 2025–2030

Scope: Focuses on sustainable, green GCCs in GIFT City, Ahmedabad and Surat, targeting semiconductors, fintech and engineering R&D.

Targets: 200 GCCs with emphasis on high-IP value addition; unspecified job figures but aligned to $10B exports.

Key incentives: Green building certifications subsidised; tax rebates on ESG compliance; SEZ extensions for GCCs.

Value propositions: GIFT City’s IFSC status for finance GCCs; port-led exports; renewable energy availability.

Limitations: High initial setup costs in GIFT; talent poaching by Mumbai/Pune; water scarcity risks.

Impact: Drove 15% growth in fintech GCCs; integrated with the national semiconductor mission.

Maharashtra GCC Policy 2025

Scope: Builds on existing GCCs in the Mumbai-Pune corridor for data-intensive operations like AI/ML and cybersecurity.

Targets: Double GCC footprint to 800+; add 200,000 jobs via tech park expansions.

Key incentives: Reliable power tariffs; data centre colocation subsidies; fast-track environmental clearances.

Value propositions: Mature infra (50% of India’s data centres); finance-IT synergy; diverse talent from IITs/IIMs.

Limitations: Highest real estate costs; urban congestion; regulatory overlaps with central policies.

Impact: Retained leadership with 25% national GCC share; facilitated $5B expansions in 2025.

Telangana GCC Policy 2024–2025

Scope: Hyderabad-centric for ITES, pharma-tech and AI GCCs, leveraging T-Hub and Genome Valley.

Targets: 300 new GCCs; 150,000 jobs; $20B revenue by 2029.

Key incentives: 15% capital subsidies; SGST reimbursements; R&D grant matching.

Value propositions: Pharma-IT convergence; startup ecosystem (3rd largest globally); robust HYD airport.

Limitations: Peak power/water shortages; high employee attrition; flood-prone outskirts.

Impact: Hosts 200+ GCCs (10% national); $4B investments in 2025 alone.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Sanjay Srivas https://orcid.org/0009-0004-3527-9758

Bagri, P., Prakash, Y., Ray, A., & Khandelwal, P. (2024). Evolution of global capability centres (GCCs) in India: Lessons for setting up, scaling, and transforming businesses. SSRN. https://doi.org/10.2139/ssrn.4921764

Cyrill, M., & Anand, K. (2023, August 6). How India is gearing up for a US$110b GCC industry by 2030. EY. Retrieved, 9 February 2026, from https://www.ey.com/en_in/insights/consulting/global-capability-centres/how-india-is-gearing-up-for-a-us-110b-dollars-gcc-industry-by-2030

GCC Policy 2024. (n.d.). Government of Karnataka. Retrieved, 18 September 2025, from https://eitbt.karnataka.gov.in/uploads/media_to_upload1732030878.pdf

Ghosh, S. (2025, March 21). India’s role in the future of GCCs or captive centers. Retrieved, 9 February 2026, from https://inductusgcc.com/shaping-the-future-of-captive-centers-or-gccs-indias-leading-role/

IBEF. (2024, October 18). Global capability centres shaping India’s corporate growth. Retrieved, 9 February 2026, from https://ibef.org/blogs/global-capability-centres-are-transforming-india-s-corporate-landscape

Jha, S. K., & Seth, A. (2025). Global capability centres: Emerging opportunities and challenges. IIMB Management Review. https://doi.org/10.1016/j.iimb.2025.100595

Jones Lang LaSalle. (2024). GCC surge: 1,800+ centres occupy over 240 mn sq. ft. Retrieved, 9 February 2026, from https://www.jll.com/en-in/newsroom/gcc-surge-1800-plus-centres-occupy-over-240-mn-sq-ft.html

NASSCOM. (2025, September 13). India’s unique value proposition: An ecosystem for scalable innovation through global capability centers. Retrieved, 9 February 2026, from https://community.nasscom.in/index.php/communities/global-capability-centers/indias-unique-value-proposition-ecosystem-scalable-innovation

Ojha, R., Gangrade, D., Dwivedi, M., & Narsalay, R. (2025). Catalysing value creation in Indian global capability centres. PwC. Retrieved, 9 February 2026, from https://www.pwc.in/catalysing-value-creation-in-Indian-global-capability-centres.html

Phadnis, S. (2024, August). How global capability centres are powering India’s job market. The Times of India. Retrieved, 9 February 2026, from https://timesofindia.indiatimes.com/business/india-business/how-global-capability-centres-are-powering-indias-job-market/articleshow/112577023.cms

PwC. (2023). Six imperatives to scale up the global capability centre market in India. Retrieved, 9 February 2026, from https://www.pwc.in/research-and-insights-hub/six-imperatives-to-scale-up-the-global-capability-centre-market-in-india.html

Reddy, C. A. M.-B., & Jain, A. (2024, March 27). Strategic structuring and modelling global capability centres (GCCs) in India: How to set up. Lexology. Retrieved, 9 February 2026, from https://www.lexology.com/library/detail.aspx?g=f65aed1f-25cf-4bfb-933e-bc82be9aba66

The Times Group. (2024). India becomes leading GCC leader with more than 1800 centers. The Times of India. Retrieved, 9 February 2026, from https://timesofindia.indiatimes.com/business/india-business/india-becomes-leading-gcc-leader-with-more-than-1800-centers/articleshow/114515273.cms

Yadav, K. (2025). Human capital in India: A global capability centre (GCC) conundrum. International Journal of Innovations & Research Analysis (IJIRA), 5(2), 27–34.