GLIMS Journal of Management Review and Transformation

Search

Search

Mohsina Dawood1, Zia ul Haq1 and Muzamil Ahmad Baba2

1Department of Management Studies, Central University of Kashmir, Jammu and Kashmir, India

2Institute of Public Enterprise, Hyderabad, Telangana, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This article examines the link between perceived benefits, perceived risks and continuance intention of using mobile banking applications through the transmission mechanism of user satisfaction. The primary mode of data collection, comprising a structured questionnaire, was used, and a sample of 422 respondents belonging to the union territories of Jammu & Kashmir (J&K) and Ladakh was chosen. The mobile banking applications, namely Yono and Mpay Delight of two reputed banks, namely the State Bank of India and the Jammu & Kashmir Bank Ltd., respectively, were considered for study. Structural equation modelling and an independent samples t-test were used for analysing data. The results of the research study depicted a significant and positive effect of perceived benefits and user satisfaction, and a negative impact of perceived risks on continuance intention of using mobile banking applications. Moreover, user satisfaction partially mediated the link between perceived benefits and continuance intention. This study provides a fresh perspective for managerial practices to comprehend the crucial elements pertaining to users’ desire to stick with mobile banking applications. This research advocates that engineering managers should provide straightforward and easy-to-use technology to increase the rate at which mobile banking applications are maintained. Furthermore, the findings suggest the crucial role of mobile banking in encouraging financial inclusion, thereby contributing to economic development. In this digital age, banks that provide mobile banking services may find strategic value in the study’s conclusions.

Mobile banking, perceived benefits, perceived risks, Mpay Delight, Yono SBI, structural equation modelling

Introduction

Technology is seen as the cornerstone of today’s rapidly changing world, which is developing at an alarming rate. Technology has permeated every part of our lives, as seen by its development and applications. Many jobs are now finished electronically due to the extensive use of information and technology at work and at home. As a result, time and location are no longer significant to various trades, making the internet a truly global marvel. Our daily lives have been impacted and transformed by the expansion and development of the internet and information technology (Mladenovic & Krajina, 2020; Raudeliuniene et al., 2018).

With the introduction of this wonder, practically every industry changed. The financial industry also began making large investments in this technology after realising its importance. Because banks needed to automate their operations to meet the ever-increasing demands of their customers and keep up with the technological changes occurring globally, the ‘evolution of electronic banking that started from the use of automatic teller machines (ATM) and passed through telephone banking, direct bill payment, electronic fund transfer, and the revolutionary mobile banking’ was the outcome (Baabdullah et al., 2019). Banks serve their clients’ diverse requirements and desires, which are becoming more and more specific (Komulainen & Saraniemi, 2019). Online banking, mobile banking, and near field communication are some of the technologically oriented delivery platforms that banks use to provide banking services (Shankar et al., 2020).

Mobile banking was the most significant change that represented a significant departure from traditional banking among the positive innovations brought forth by the banking industry. It is regarded as the most valuable and adaptable business application currently available (Singh & Srivastava, 2018), whose rise can be ‘ascribed to technological advancement and evolving consumer demands in terms of affordability, flexibility, choice, and convenience’ (Chawla & Joshi, 2017).

As cited by Mullan et al. (2017), Mobile banking is defined as ‘A transaction in which a client connects to the service provider through a mobile gadget, like a smartphone or Personal Digital Assistant’. Through the extension of remote correspondence, mobile banking has made it easier to develop and expand commercial transactions. It has also created a wide range of business opportunities by making it easier to trade, acquire goods and services, pay bills, and conduct fund transactions. This advancement has not only improved the bank’s operations in terms of staff workload reduction, catering time reduction, digital device use, and customer acquisition, but it has also made customers’ daily banking activities more convenient, which is why the industry is moving toward digitalisation. Thus, researchers’ assertion that this banking administration approach has paved the way for innovative economic advancement in both wealthy and developing nations is supported.

Mobile banking is a great example of a mobile technology innovation in the banking industry, allowing customers to independently conduct financial transactions (such as checking their balance, transferring funds, or paying bills) using smartphones, PDAs, or mobile devices at any time and location of their choosing. (Alalwan et al., 2017)

Furthermore, increased smartphone usage has increased interest in M-banking services, leading nearly all financial institutions to provide this ground-breaking service along with a new suite of goods and apps designed to increase their clientele (Mohammed & Rozsa, 2024). Therefore, the mobile phone has become an essential tool for banking clients’ daily tasks.

When the internet revolution became apparent in the late 1990s, the idea of mobile banking was developed. The first service was initiated and launched by a German company called Pay-box in collaboration with Deutsche Bank (Shaikh & Karjaluoto, 2015). Banks in India have been particularly competing with one another to adopt innovation in order to provide and improve better customer services and to move toward a computerised shift in order to stay competitive.

For this reason, banks must look into mobile banking trends to comprehend the market and stay ahead of the competition. However, numerous financial institutions have made an effort to integrate this innovation into their banking procedures throughout time. According to industry projections, India is becoming the fastest-growing portable market (Chawla & Joshi, 2017), with advertisers projecting growth of over 75% of the population by the end of 2025 (Global System for Mobile Communications, 2018). Analysts must give this rapidly changing consumer of the massive mobile banking sector considerable thought. Since India was a latecomer to the demonetisation wave, the Central Government and the nation’s financial regulatory body have focused on facilitating an ever-increasing number of cashless transactions.

Numerous industries, including banking, have seen changes as a result of the widespread adoption of mobile phones, the creation of smartphones, and the more affordable, generally available internet (Domazet et al., 2018). Because of this, a growing number of banks, software firms, microfinance organisations, and service providers are now providing this innovative service in addition to new product and application sets meant to enhance client retention, boost market share, expand their clientele (including to unbanked populations), increase operational efficiency, and create new job opportunities (Shaikh, 2013). Banking is a highly regulated industry with relatively stable business models and significant transaction and operating costs. In a developing market like India, mobile banking still has a long way to go. Banks and Financial institutions have been focusing on cashless transactions, and the majority of banks have already released fully secure mobile banking software and applications.

Numerous research studies have used both qualitative and quantitative methodologies to examine M-banking and related aspects that affect customers’ adoption of it. It is possible for someone who used a certain technology in the first phase to quit using it for a variety of reasons. In their analysis of the factors influencing users’ continuing intention to use (CI) of mobile banking technology, Foroughi et al. (2019) discovered that users will only stick with mobile banking if they find it helpful and are happy with their experience. Customers believe that using mobile banking is justified when the advantages (like convenience, cost savings or performance) outweigh the risks (like fraud involving transaction integrity or authenticity, reputational harm, privacy or confidentiality breaches; Chang et al., 2016). Therefore, it is critical to comprehend the benefits and risks of mobile banking from the viewpoint of the user.

There is not much peer-reviewed literature on mobile payments, even if the number of papers has increased. Numerous studies on mobile banking have been published in recent years due to the FinTech industry’s explosive expansion and the complexity of the factors impacting its use and adoption. Recent research indicates that numerous articles have looked at the components that have a bearing on the results, consumer approval, and adoption of different mobile payment platforms, particularly following the COVID-19 pandemic, as well as customer satisfaction, security concerns, design features, and innovation (Al-Qudah et al., 2022; Dahlberg et al., 2015; Makki et al., 2016).

There is a dearth of literature on the usage of M-banking apps in India, particularly in J&K and Ladakh. Therefore, the current study intends to assess the use of different mobile banking apps of select banks operating in J&K and Ladakh. The study would provide implications for various stakeholders, namely, banks, the government, and customers, by making thorough research on the use of mobile banking applications. As the leading financial institutions in the union territories of J&K and Ladakh, the State Bank of India and the J&K Bank have also launched the high-end applications, ‘Yono’ and ‘Mpay Delight’, respectively. However, M-banking is still relatively new in J&K and Ladakh compared to online banking; hence, the bank’s job is to make it more appealing to clients to recognise using the mobile channel for banking services. Yono is a mobile application introduced by the premier institution of India, namely the State Bank of India. There are 250 computerised SBI branches across J&K and Ladakh. Mpay Delight is a mobile application introduced by the most prominent bank, namely J&K Bank, in the UT of J&K and Ladakh. The said bank owns a wide network of 1,001 computerised branches across J&K and Ladakh. Given their clientele, the research has a lot of room to grow because these banks are leading the way in the valley’s transition to a digital economy. J&K and Ladakh are perfect locations for the study because of the high percentage of mobile users, the rapid expansion of m-commerce, and the clients’ preference for more modern banking services.

The current study was carried out in order to learn how users react to mobile banking, especially in light of the lack of adequate banking services, especially in remote areas, and the periodic interruptions of banking services for a variety of reasons. Given that the Kashmir Valley has been a region plagued by conflict over the past 30 years, with regular strikes and the occasional suspension of banks and other commercial facilities, the current study is especially important. Customers can choose to use mobile banking to get uninterrupted financial services whenever it is convenient for them, which will help them get out of this unpleasant scenario. Nevertheless, in spite of everything, there does not appear to be any favourable reaction to the customers’ usage of M-banking. In order to resolve the concerns, a comprehensive investigation is required to determine the causes of any potential inhibition, hesitation, internet troubles, or ignorance among mobile users regarding the usage of mobile banking in general.

The current research is being conducted with the following objectives:

The primary source of data collection was used comprising of a well-structured questionnaire to attain the specific objectives of the research. These research questions are at the centre of the primary research problem that motivates our investigation: (a) How much (if at all) does the likelihood that users will continue (or stop) using mobile banking applications depend on their perceptions of the risks and benefits? (b) To what extent (if at all) do user-perceived benefits and the satisfaction of consumers play a vital role in using mobile banking applications?

A review of the literature on the impact of several prognosticators on the intention to continue using mobile banking applications is included in the next portion of this research study. The study framework and the formulation of the hypotheses are based on the literature review. The section addressing the study sample’s descriptive statistics and methods, along with its variables, comes next. The results are next discussed, and then the conclusions, limitations, implications, and future directions of the research are covered.

Literature Review and Hypothesis Development

Theoretical Background of Mobile Banking

Scholars have defined mobile banking differently and used a variety of terminologies to describe it. Liu et al. (2009) have referred to it as M-banking, Ivatury and Mas (2008) termed it as branchless banking, and Donner and Tellez (2008) called it M-finance. Muñoz-Leiva et al. (2017) described it as a remote service provided by financial organisations to meet the needs of their clients via mobile devices, PDAs, tablets, etc., whereas Tam and Oliveira (2017) proposed that ‘M-banking is a service or product offered by financial institutions that makes use of portable technologies’. Accordingly, this study defines M-banking as a platform that allows users to access information associated with their bank accounts and conduct financial transactions using a mobile device at any time and from any location. Over time, a variety of theoretical stances have emerged, including well-known models to examine the adoption of mobile banking, such as the Unified Theory of Acceptance and Use of Technology (UTAUT) by Venkatesh et al. (2003), the Task-technology Fit by Goodhue and Thompson (1995), the Technology Acceptance Model (TAM) by Davis (1989), the Social Cognitive Theory by Bandura (1989), and the Innovation Diffusion Theory (IDT) by Rogers (1983).

Perceived Benefits and Continuance Intention of Using Mobile Banking Applications

Relatively little research has been conducted on continuance intention in comparison to the bulk of studies on initial adoption. It was confirmed that the intention to continue using mobile internet services was influenced by perceived enjoyment, familiarity, utility, uncertainty avoidance, and access quality (Lee et al., 2007; Shin et al., 2010; Zhou, 2011). Likewise, researchers have discovered that consumers’ intentions to stick with mobile data services can be influenced by elements like perceived enjoyment, social impact, information quality, and perceived cost (Choi et al., 2011; Kim, 2010; Kim et al., 2009). Chen (2012) proposed that the intention to stick with mobile banking is significantly influenced indirectly by service quality and technological preparedness. According to Chen (2012), users’ expectations are positively impacted by the ongoing development of mobile content services. According to Kang et al. (2012), three key factors that influence long-term M-banking use are perceived value, channel preference, and usability.

The influence of service quality and justice on the happiness of users, which in turn influences the intention to continue using mobile value-added services, was investigated by Zhao et al. (2012). They investigated how user satisfaction is impacted by service quality and fairness, and how this influences users’ intentions to continue using mobile value-added services.

Thus, we formulated the hypotheses as:

H1: Perceived benefits have a positive impact on continuance intention to use mobile banking applications.

User Satisfaction and Mobile Banking Continuance Intention

In order to determine which elements need to be addressed in order to enhance the system’s service quality and, consequently, please consumers, researchers are also investigating how satisfied users are with mobile banking (Khan et al., 2018).

User satisfaction is a critical and potent response to purchase situations in retail banking. Numerous scholarly studies indicate that satisfaction with mobile banking is a component that affects its results (Mohammadi, 2015; Püschel et al., 2010). The idea of net valence states that customers should only utilise a product or service if they feel the benefits outweigh the risks in order to maximise the product’s or service’s net value (Featherman et al., 2006; Li & Wang, 2017). Because they have a positive attitude toward a product or service, consumers are more likely to use it when they intend to (Fishbein & Ajzen, 1975). According to this hypothesis, the belief that the benefits of a product or service outweigh the drawbacks is the foundation for the intention to keep using it (Yousafzai et al., 2010). In their examination of consumers’ inclination to utilise (and persist in utilising) mobile payment systems, Qasim and Abu-Shanab (2016) clarified that consumers’ propensity to use mobile banking is influenced by their perceptions; therefore, the more highly they value a product or service, the more likely they are to use it. Accordingly, it is hypothesised as:

H2: User satisfaction bears a positive influence on continuance intention to use mobile banking applications.

Perceived Risks and Continuance Intention of Using Mobile Banking Applications

The results of Alonso-Dos-Santos et al. (2020) revealed that there exists a strong relationship between perceived risk and mobile banking usage. According to net valence theory, users perceive a number of risks associated with utilising mobile banking, including operational, legal, security, and financial risks. Perceived risk is a significant aspect in e-banking that indicates a user’s intention to continue using a product or service (Arner et al., 2015). Due to the growing global context of mobile banking, the most recent study in the field by Marafon et al. (2018) indicated that the analytical model needs to be improved, particularly in order to comprehend the relationship between intention to use mobile banking and perceived risk. Real or perceived hazards or challenges related to a product or service, like mobile banking, lead to negative views that deter use (Britton et al., 2019). Research on innovation, information systems, and consumption indicates that if consumers perceive a risk involved in using IT services, their intentions to do so are negatively influenced (Zhou, 2015). Zhou examined the advantages and disadvantages of location-based services from the perspectives of enablers (benefits of usefulness and trust) and inhibiters (privacy risks). The results showed that propensity to use a product or service was correlated with perceived benefits (like trust), outweighing risks. He did this by using the dichotomy of facilitators and inhibitors to evaluate the elements that influence the uptake of location-based services. Wu and Wang (2005) discovered that behavioural intentions in e-commerce are significantly influenced by perceived risk. According to various studies, one of the primary factors influencing users’ acceptance of M-banking is perceived risk (Brown et al., 2003; Luarn & Lin, 2005). Therefore, it is hypothesised that:

H3: Perceived risks have a negative impact on continuance intention to use M-banking applications.

User Satisfaction as a Mediator Between Perceived Benefits and Continuance Intention to Use M-banking Applications

Satisfaction has a mediating role between application continuing intention and hedonic advantages. Additionally, the relationship between application continuing intention and utilitarian gains is mediated by satisfaction (Akel & Arma.png) an, 2021). The relationship between different customer-perceived benefits, including learning, self-realisation, and hedonic benefits, and the intention to continue in online China brand communities is mediated by satisfaction (Han et al., 2018). Based on the above literature, it is hypothesised that:

an, 2021). The relationship between different customer-perceived benefits, including learning, self-realisation, and hedonic benefits, and the intention to continue in online China brand communities is mediated by satisfaction (Han et al., 2018). Based on the above literature, it is hypothesised that:

H4: User satisfaction mediates the relationship between perceived benefits and continuance intention to use M-banking applications.

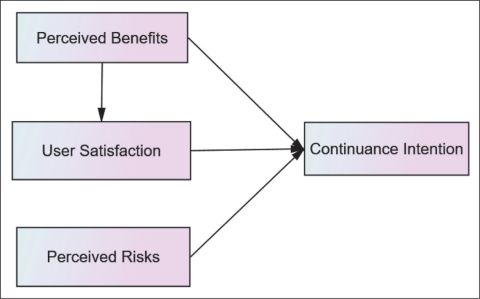

Based on the objectives of the study and the proposed study model (Figure 1), further hypotheses were framed as:

Figure 1. The Proposed Research Model.

H5: A significant difference occurs between Mpay and Yono users with respect to perceived benefits.

H6: A significant difference occurs between Mpay and Yono users with respect to user satisfaction.

H7: A significant difference occurs between Mpay and Yono users with respect to continuance intention.

H8: A significant difference occurs between Mpay and Yono users with respect to perceived risks.

Research Methodology

Population and Sample

The proposed study is delimited to the mobile banking applications of select banks operating in Jammu and Kashmir. The data was collected from customers of the select banks operating in Jammu and Kashmir. A questionnaire survey was used to perform this cross-sectional investigation. The main method of data analysis was structural equation modelling (SEM), which uses a two-step process that combines measurement and structural models to concurrently create a graphical depiction of the research relationships. Also, an independent samples t-test was used to check the difference between two mobile banking applications in different aspects covered under the objectives of the study.

This study was conducted between September 2024 and February 2025. The usage of mobile banking applications is increasing day by day. As such, many banks are providing mobile banking services to their customers to satisfy their changing requirements (Etikan et al., 2016). We selected convenience sampling because it is widely accepted in the social sciences and ensures timely availability and accessibility, geographical vicinity, and respondents’ willingness to participate. The lack of a suitable sample frame led to the adoption of convenience sampling, which allowed researchers to collect data that would have been impossible otherwise.

The population targeted comprised employees working in different public and private organisations, professionals, businessmen, students and scholars belonging to the union territories of J&K and Ladakh. The non-probability sampling method of snowball sampling was employed to gather responses because it was difficult to reach such a broad group of interest. Questionnaires were physically distributed among the respondents. Participants were made aware of the purpose of the study prior to the survey being administered.

The sample size for the study was calculated as per Krejcie and Morgan’s (1981) formula, as 384, as the total population exceeded 10 lakhs. The total number of 422 questionnaires was distributed, taking the attrition rate of 10%. Twenty-two questionnaires were omitted from the study due to incomplete replies. As a result, only 400 questionnaires were deemed suitable for the data analysis.

Research Design

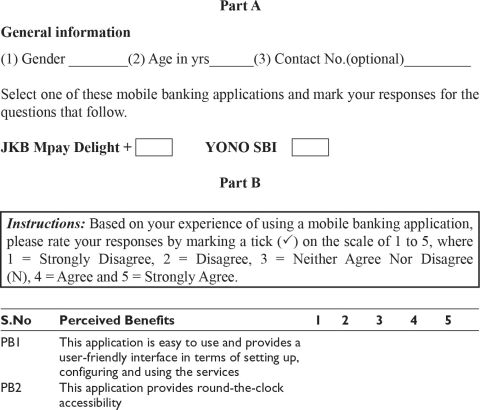

The survey questionnaire was divided into two sections: the first portion gathered demographic data from the respondents, while the second part contained information regarding the study constructs (refer to Appendix A). Below is a comprehensive overview of these two sections:

The participant’s age and gender were ascertained in the first segment.

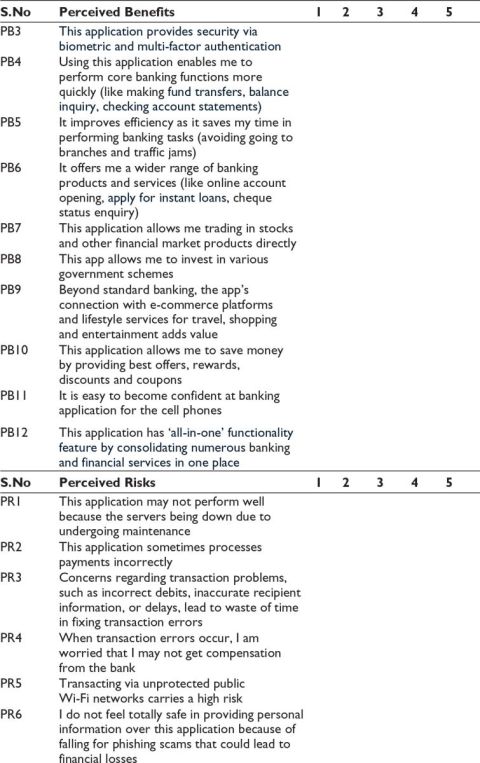

The second section involves: Perceived benefits -this construct was measured using Rahim’s twelve-item scale (Abdul-Rahim et al., 2022). This scale’s representative item is, ‘This application is user-friendly in terms of setting up, configuring and using the service’.

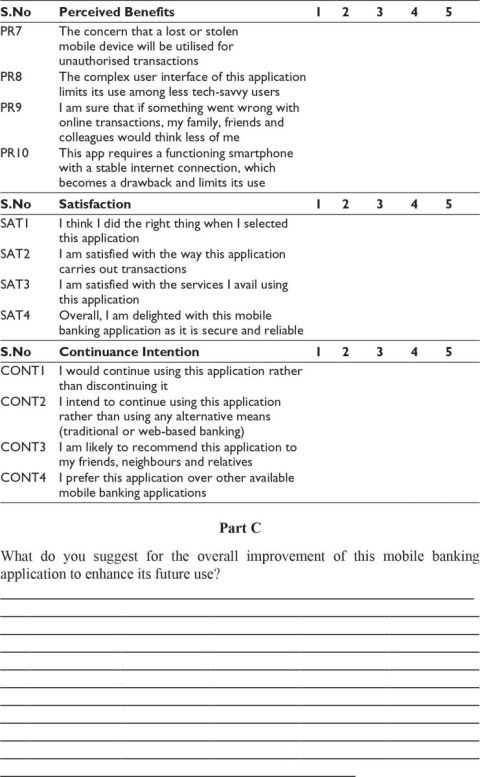

User satisfaction: A four-item scale was adapted from Geebren et al. (2021) to measure the user satisfaction construct. This scale’s sample item is, ‘I think I did the right thing when I selected this application’.

Perceived risks: A 10-item scale adapted from Lee (2009) was used to assess the perceived risks of the mobile banking construct. This scale’s representative item is, ‘This application may not perform well because of servers being down due to undergoing maintenance’.

Continuance intention: Poromatikul et al. (2020) provided a four-item scale, which we modified to assess the continuing intention construct. This scale’s sample item is, ‘I would continue using this application rather than discontinuing it’.

In order to document respondents’ responses about the study items, a 5-point Likert scale was employed, with 1 denoting strongly disagree, and 5 denoting strongly agree. The study variables were confirmed using a pilot study comprising 30 respondents before the final data collection. To examine the links between the study variables, a confirmatory factor analysis (CFA) (using AMOS 24.0) is conducted after an exploratory factor analysis (EFA) (using SPSS 27.0). Additionally, the average variance retrieved, CR, and squared correlations were used to confirm the validity and reliability of the study components.

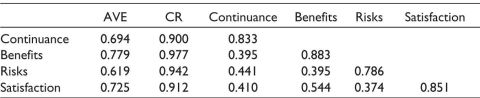

Reliability and Validity

The reliability was assessed using composite reliability (CR) and convergent validity using average variance extracted (AVE) (Table 1). Reliability is indicated by the composite reliability estimates above 0.70 values, which is the minimal criterion (Zafiropoulos et al., 2012). In order to evaluate dependability, this study gave CR values precedence over Cronbach’s alpha because the latter can provide biased findings (Peterson & Kim, 2013). Furthermore, when evaluating reliability, the CR is superior to Cronbach’s alpha. Since the AVE values are higher than the 0.50 level, or the lowest threshold level, the results also show convergent validity (Fornell & Larcker, 1981).

Table 1. The Average Variance Extracted (AVE), Composite Reliability (CR) and Shared Variance Estimates.

We adhered to Fornell & Larcker’s (1981) suggestion that the AVE estimates of any two constructs be greater than the shared variance estimate (squared correlations) in order to guarantee discriminant validity. Since the AVE estimates for each factor are greater than their corresponding squared correlations, the results demonstrate discriminant validity (Table 1).

Therefore, the above results indicate the reliability and validity of the dataset.

The Descriptive Statistics of the Study Sample and Its Variables

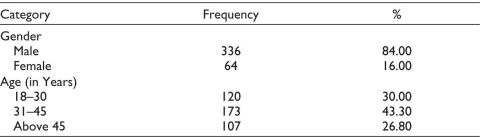

Respondents Demographic Profile

Most respondents were male, that is, 84%, followed by females, 16%. Regarding age, 30% of the respondents belonged to the 18–30 years; 43.30% were from 31 to 45 years age group, followed by those above 45 (26.80%) (see Table 2).

Table 2. The Demographic Information.

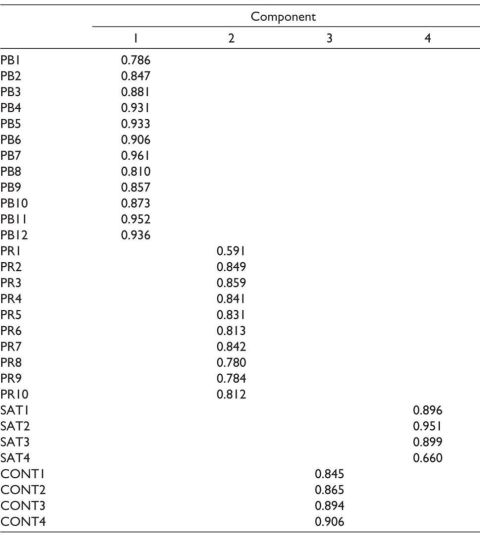

Exploratory and CFA

Principal components analysis with Promax rotation was employed in EFA to investigate the study constructs. According to the EFA results, every item had loadings greater than 0.6 on its corresponding factor (see Table 3). Furthermore, according to Ford et al. (1986), factor loadings higher than 0.4 lessen subjectivity in the interpretation of data. The validity of the study constructs is thus indicated by the EFA results.

Table 3. Pattern Matrix.

Notes: Extraction Method: Principal Component Analysis. Rotation method: Promax with Kaiser normalisation.

aRotation converged in five iterations.

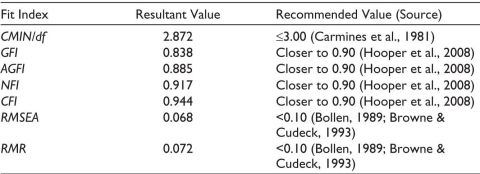

Also, CFA was used to validate the factor structure that was taken from EFA. For reliable outcomes, it is essential to have higher model-fit values (Moslehpour et al., 2018). According to the findings, every fit index met the suggested threshold values (see Table 4). As a result, the study’s suggested model aligns well with the empirical data.

Table 4. The Model-fit Summary.

Hypothesis Testing

Structural Equation Modelling

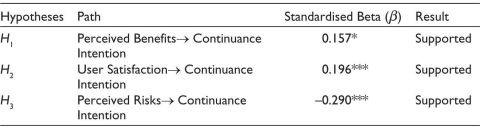

SEM was employed for testing the study’s proposed hypotheses (H1 to H3). Research model compatibility is confirmed, and causal linkages are assessed through the use of SEM (Tobbin, 2010). In the structural model, the path coefficients are represented by the standardised betas (β) (Saadé & Bahli, 2005). Furthermore, since the correlations between the independent variables were less than 0.8, there were no problems with multicollinearity.

The results show that the model explains cumulative variance of 75.61%, with 44.61% of the variance in perceived benefits, 16.95% in perceived risks, 7.99% in user satisfaction, and 6.03% in Continuance intention. The findings validated the hypothesised connections regarding H1, H2, and H3 (Table 5).

Table 5. Structural Model Coefficients (Hypothesis Testing: H1 to H3).

Note: ***p < .001; *p < .05.

Mediation Analysis Using Hayes Approach

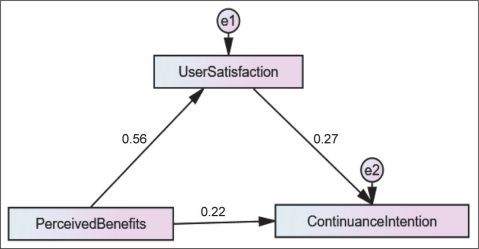

According to several researchers, SEM is the best method for examining the mediation effect in any study (Baron & Kenny, 1986; Frazier et al., 2004; Hoyle & Smith, 1994; Preacher & Hayes, 2004). This is because it liberates the mediator and the dependent variables from their measurement mistakes; if they are not included, the correlation between the variables is diminished. By examining numerous independent and dependent variables at once, SEM is also far more adaptable and examines the complete causal model. In the present study, mediation analysis has been used to examine whether the causal effect of perceived benefits on continuance intention of using mobile banking applications is caused by user satisfaction (refer to Figure 2). Preacher and Hayes (2004) state that determining whether the indirect pathway from independent variable to mediator to dependent variable is statistically significant is a prerequisite for obtaining evidence in favour of mediation. With this method, the overall impacts are divided into direct and indirect effects.

Figure 2. The Mediation Model.

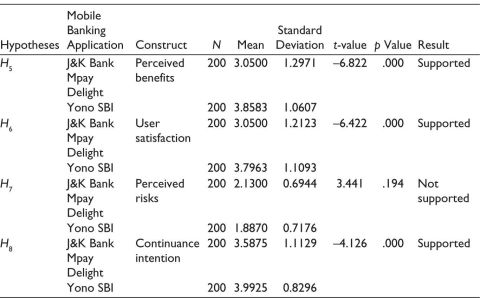

Independent Sample t-test.

An independent sample t-test has been performed to assess the disparity between the means in two unrelated groups, that is, whether the mean value of the test variables (perceived benefits, user satisfaction, perceived risks and continuance intention) for one banking application, namely J&K Bank Mpay Delight differs significantly from the mean value for the other one, that is, Yono SBI. The results of the test are depicted in Table 7.

Findings and Discussion

This study explored the continuance intention of mobile banking applications through the perceived benefits, user satisfaction and perceived risks mechanisms. Existing models were used to accommodate the research constructs. The constructs included perceived benefits, user satisfaction and perceived risks as the antecedents and continuance intention as the outcome variable. The inclusion of user satisfaction as the intermediary variable in the current research model strengthens the validity of the study’s conclusions, as responsiveness and security features have a big impact on people’s acceptance of technology (Barnes & Vidgen, 2002; Parasuraman et al., 1985).

Our results support H1, that is, a significant positive relationship between perceived benefits and continuance intention (β = 0.157; p < .05). This finding supports prior studies (Looney et al., 2004) and signifies that the more benefits offered by mobile banking applications to the users, the greater their willingness to continue with the mobile application. Moreover, Additionally, this emphasises how crucial it is to promote mobile banking’s benefits to guarantee its continued growth and use (Baganzi & Lau, 2017). Further, H2, a significant and positive association between user satisfaction and continuance intention, is also supported (β = 0.196; p < .001). This finding supports the existing literature (Mohammadi, 2015; Püschel et al., 2010). It may be because when the users are highly satisfied with the services of a mobile banking application, their continuance intention of using the application would also be positive. Because happy customers are more likely to intend to make additional purchases in the future, happiness has thus historically been recognised as an antecedent (Chiang et al., 2008).

H3, a negative relationship between perceived risks and continuance intention of using mobile banking application, is also supported (β = –0.290; p < .001). The financial, performance, security/privacy, time and social risk of mobile banking adversely affect its continuance intention to use. This finding also aligns with the literature (Abrahao et al., 2016; Alonso-Dos-Santos et al., 2020; Lee, 2009; Zhou, 2015). As depicted in Table 6, the perceived benefits exert their effect on continuance intention both directly and indirectly. There is partial mediation of user satisfaction between perceived benefits and continuance intention, indicating significant values (β = 0.218; p < .001) and (β = 0.149; p < .001) for both direct and indirect effects, respectively. We can conclude that there is a positive effect of both perceived benefits and user satisfaction on continuance intention of using mobile banking applications. This aligns with the previously established literature (Akel & Armaan, 2021; Han et al., 2018). The user satisfaction does not fully mediate the perceived benefits and continuance intention relationship.

Table 6. The Mediation Results (Hypothesis Testing: H4).

As depicted in Table 7, the findings of the study reflect that there is a significant difference in perceived benefits with respect to Mpay Delight and Yono with (t = –6.822, p < .001). Hence, H5 is accepted. It was found that the Yono provides more benefits in comparison to Mpay Delight. There is also a significant difference in user satisfaction with respect to Mpay Delight and Yono (t = –6.422, p < .001). Hence, H6 is also accepted. User satisfaction was more prominent in case of Yono users than Mpay users. With respect to perceived risks regarding Mpay Delight and Yono (t = 3.441, p = .194), indicating there is no significant difference between the two groups. Therefore, H7 is rejected. It was seen that there is a slight difference in the perceived risks of both Yono and Mpay Delight. There is a significant difference in continuance intention between Mpay Delight and Yono with (t = –4.126, p < .001), thereby leading to acceptance of H8. The intention of users to continue using Mpay Delight was found to be negative as compared to those using Yono.

Table 7. Independent Samples t-test for Perceived Benefits; User Satisfaction, Perceived Risks and Continuance Intention with Respect to Mobile Banking Applications (Hypothesis Testing: H5 to H8).

Implications

Theoretical Implications

This research study proposed and tested a mobile banking continuance model in the Indian context. This study explored the continuance intention of mobile banking applications through the perceived benefits, user satisfaction and perceived risks mechanisms. First, the results of the study contribute to the understanding and explanation of the prognosticators of technology adoption by advancing the TAM and UTAUT models, especially mobile banking continuance (Davis, 1989; Venkatesh et al., 2003). Second, our study results show that perceived benefits and user satisfaction together play a vital role in enhancing and maintaining continuity with mobile banking applications of different users. These benefits include convenience, ease of use, security, privacy, control, customisation, interactivity, and so on (Alalwan et al., 2016).

Furthermore, on account of findings of the study, it is inferred that risks perceived by users in terms of poor performance of banking applications on account of servers being down due to ongoing maintenance, fear of losing money due to information leakage, and so on, affect the continuance intention of users. In this regard, banking organisations should focus on improvement in facilitating hassle-free service to their customers, such as minimising the updating time for applications, leading to the least interruption of server operations and superior performance. Also, the banks can enhance security measures and develop trust of their users by introducing biometric technology such as facial mapping, fingerprint and voice recognition.

Practical Implications

Regarding technology (mobile banking) suppliers and users, including the Indian financial services sector, our findings also have some ramifications for managers and regulators. Furthermore, this study sheds light on the core priorities of users regarding M-banking usage and continuity. For engineering management practice, this study has some commendable implications. For instance, this study highlights that engineering managers should simplify mobile banking applications to increase their use and retention rate by creating solutions that are user-friendly and beneficial.

Moreover, our study signifies that J&K Bank engineering staff need to focus on technology specifications for stimulating tech continuance. Many respondents using Mpay Delight reported that giving both transaction personal identification number (TPIN) and mobile personal identification number (MPIN) details, waiting for one-time password (OTP) while making a simple transaction, becomes tedious for users. It adversely affects the continuance intention of users and makes them switch to other applications. Therefore, when it comes to mobile banking, engineering managers should put an emphasis on added value and simplicity. Enhancing technology’s usability, cutting down on time waste, and speeding up transactions are all examples of the simplicity perspective, which is connected to the added value perspective.

To enable user-friendly products, technology providers can concentrate on improving the general user interface (UI) of their solutions. In order to help project managers, system developers, and human factor engineers, Opaluch and Tsao (1993) provided 10 ways to enhance usability engineering. Identifying end users, appointing a UI designer early on, and listing end-user tasks are some of these strategies. Furthermore, by increasing awareness of its features and advantages, mobile banking service providers can encourage users to keep using it. It becomes crucial to be aware of a new technology since its acceptance is preceded by user (organisation or individual) knowledge about how simple (easy-to-use) and valuable the technology is. To achieve the desired goal, internal marketing initiatives should concentrate on encouraging word-of-mouth advertising. This implies that customers must be aware of the advantages and capabilities of mobile banking in order to support its continuity. Furthermore, as mobile banking has been viewed as a promising element in this field, it is imperative that both the public and commercial sectors support it to assist India in achieving the goal of financial inclusion. To summarise, our study offers a candid view for banking organisations on improving the performance and overall continuance of their mobile banking applications.

Conclusion

This study is the first to explore the role of perceived benefits, user satisfaction, and perceived risks in influencing continuance intention of mobile banking applications in the union territories of J&K and Ladakh. The applications of two reputed banks, namely the State Bank of India and the Jammu & Kashmir Bank Ltd., have been taken into consideration. By incorporating these research constructs into the usage and continuation of mobile banking, this study contributes to the body of literature on TAM/technology acceptance theories.

Summarising the findings, it can be concluded that both J&K Bank and SBI are doing their best to deliver better mobile banking services to their customers. But J&K Bank needs to work a bit harder to improve the efficacy of Mpay Delight, as has been found from the study results that many Mpay Delight users are switching to other mobile banking applications rather than continuing with the same one. The study recommends that engineering managers should offer simple and user-friendly technology to enhance the continuance rate of mobile banking applications. Additionally, the results emphasise the significance of mobile banking in encouraging financial inclusion, thereby contributing to economic development. Banks offering mobile banking services could use the study findings strategically in this digital era.

Limitations and Future Research Directions

This research has certain limitations despite its noteworthy achievements. First off, the quality and validity of the data were limited because this study used self-reported questionnaires, which are more likely to contain bias due to respondents concealing their genuine emotions (Fan et al., 2002). To get around this restriction, future research can concentrate on objective data. Second, this study focused on only two mobile banking applications, namely J&K Bank Mpay Delight and Yono SBI, limiting the results’ generalizability. Moreover, the area of study was confined to the union territories of J&K and Ladakh, which again raises concern for the generalizability of results. Future studies could focus on more mobile banking applications to make more assertive statements. Third, this study was cross-sectional in nature; future studies could be longitudinal in nature.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Muzamil Ahmad Baba https://orcid.org/0000-0002-0129-8860

Abdul-Rahim, R., Bohari, S. A., Aman, A., & Awang, Z. (2022). Benefit–risk perceptions of fintech adoption for sustainability from bank consumers’ perspective: The moderating role of fear of COVID-19. Sustainability, 14, 8357. https://doi.org/10.3390/su14148357

Akel, G., & Armaan, E. (2021). Hedonic and utilitarian benefits as determinants of application continuance intention in location-based applications: The mediating role of satisfaction. Multimedia Tools and Applications, 80(5), 7103–7124. https://doi.org/ 10.1080/17457823.2021.1922927

Al-Qudah, A. A., Al-Okaily, M., Alqudah, G., & Ghazlat, A. (2022). Mobile payment adoption in the time of the COVID-19 pandemic. Electronic Commerce Research, 1–25.

Alalwan, A. A., Dwivedi, Y. K., Rana, N. P., & Williams, M. D. (2016). Customer adoption of mobile banking in Jordan: Examining the role of usefulness, ease of use, perceived risk and self-efficacy. Journal of Enterprise Information Management, 29(1), 118–139.

Alonso-Dos-Santos, M., Soto-Fuentes, Y., & Valderrama-Palma, A. V. (2020). Determinants of mobile banking users’ loyalty. Journal of Promotion Management, 1–19. https://doi.org/10.1080/10496491.2020.1729312

Arner, D. W., Barberis, J., & Buckley, R. P. (2015). The evolution of fintech: A new post-crisis paradigm. Georgetown Journal of International Law, 47, 1271.

Baabdullah, A. M., Alalwan, A. A., Rana, N. P., Kizgin, H., & Patil, P. (2019). Consumer use of mobile banking (m-banking) in Saudi Arabia: Toward an integrated model. International Journal of Information Management, 44, 38–52.

Baganzi, R., & Lau, A. K. W. (2017). Examining trust and risk in mobile money acceptance in Uganda. Sustainability, 9, 2233.

Bandura, A. (1989). Human agency in social cognitive theory. American Psychologist, 44(9), 1175–1184.

Barnes, S. J., & Vidgen, R. T. (2002). An integrative approach to the assessment of e-commerce quality. Journal of Electronic Commerce Research, 3, 114–127.

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182.

Bollen, K. A. (1989). A new incremental fit index for general structural equation models. Sociological Methods & Research, 17(3), 303–316.

Britton, G. I., Neale, S. E., & Davey, G. C. (2019). The effect of worrying on intolerance of uncertainty and positive and negative beliefs about worry. Journal of Behavior Therapy and Experimental Psychiatry, 62, 65–71.

Brown, I., Cajee, Z., Davies, D., & Stroebel, S. (2003). Cell phone banking: Predictors of adoption in South Africa—An exploratory study. International Journal of Information Management, 23(5), 381–394.

Brown, M. W., & Cudeck, R. (1993). Alternative ways of assessing model fit. In K. A. Bollen, & J. S. Long (Eds.), Testing structural equation models (pp. 136–162). Sage.

Chang, L. Y., Wong, S. F., Lee, H., & Jeong, S. P. (2016). What motivates Chinese consumers to adopt fintech services: A regulatory focus theory. In Proceedings of the 18th annual international conference on electronic commerce: E-commerce in smart connected world (pp. 1–3).

Chawla, D., & Joshi, H. (2017). Consumer perspectives about mobile banking adoption in India: A cluster analysis. International Journal of Bank Marketing, 35(4), 616–636. https://doi.org/10.1108/IJBM-03-2016-0037

Chen, S. C. (2012). To use or not to use: Understanding the factors affecting continuance intention of mobile banking. International Journal of Mobile Communications, 10(5), 490–507.

Chiang, K., Zhao, W., & Yang, K. H. (2008). An empirical study on the integrated framework of eCRM in online shopping: Evaluating the relationships among perceived value, satisfaction, and trust based on customers’ perspectives. Journal of Electronic Commerce in Organizations, 6(3), 1–15.

Choi, H., Kim, Y., & Kim, J. (2011). Driving factors of post-adoption behavior in mobile data services. Journal of Business Research, 64(11), 1212–1217.

Dahlberg, T., Guo, J., & Ondrus, J. (2015). A critical review of mobile payment research. Electronic Commerce Research and Applications, 14(5), 265–284.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340.

Domazet, I., Markovi.png) , M. R., & Martinovi, A. B. (2018). Digital transformation: New challenges and business opportunities. Silver and Smith Publishers.

, M. R., & Martinovi, A. B. (2018). Digital transformation: New challenges and business opportunities. Silver and Smith Publishers.

Donner, J., & Tellez, C. A. (2008). Mobile banking and economic development: Linking, adoption, impact, and use. Asian Journal of Communication, 18(4), 318–332.

Etikan, I., Musa, S. A., & Alkassim, R. S. (2016). Comparison of convenience sampling and purposive sampling. American Journal of Theoretical and Applied Statistics, 5, 1–4.

Fan, X., Miller, B. C., Christensen, M., Park, K. E., Grotevant, H. D., van Dulmen, M., Dunbar, N., & Bayley, B. (2002). Questionnaire and interview inconsistencies exaggerated differences between adopted and non-adopted adolescents in a national sample. Adoption Quarterly, 6, 7–72.

Featherman, M. S., Valacich, J. S., & Wells, J. D. (2006). Is that authentic or artificial? Understanding consumer perceptions of risk in e-service encounters. Information Systems Journal, 16(2), 107–134.

Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention, and behavior: An introduction to theory and research. Addison-Wesley.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18, 39–50.

Foroughi, B., Iranmanesh, M., & Hyun, S. S. (2019). Understanding the determinants of mobile banking continuance usage intention. Journal of Enterprise Information Management, 32(6), 1015–1033. https://doi.org/10.1108/JEIM-10-2018-0237

Frazier, P. A., Tix, A. P., & Barron, K. E. (2004). Testing moderator and mediator effects in counseling psychology research. Journal of Counseling Psychology, 51(1), 115–134.

Geebren, A., Jabbar, A., & Luo, M. (2021). Examining the role of consumer satisfaction within mobile ecosystems: Evidence from mobile banking services. Computers in Human Behavior, 114, 106584.

Global System for Mobile Communications. (2018). Number of global mobile subscribers to pass five billion this year. Retrieved, March 19, 2026, from https://www.gsma.com/newsroom/press-release/number-of-global-mobile-subscribers-to-surpass-five-billion-this-year/

Goodhue, D. L., & Thompson, R. L. (1995). Task-technology fit and individual performance. MIS Quarterly, 19(2), 213–236.

Han, M., Wu, J., Wang, Y., & Hong, M. (2018). A model and empirical study on the user’s continuance intention in online China brand communities. Journal of Open Innovation: Technology, Market, and Complexity, 4(4), 46.

Hooper, D., Coughlan, J., & Mullen, M. (2008, September). Evaluating model fit: A synthesis of the structural equation modelling literature. In 7th European Conference on research methodology for business and management studies (Vol. 2, pp. 195–200).

Hoyle, R. H., & Smith, G. T. (1994). Formulating clinical research hypotheses as structural equation models: A conceptual overview. Journal of Consulting and Clinical Psychology, 62(3), 429–440.

Ivatury, G., & Mas, I. (2008). The early experience with branchless banking. CGAP Focus Note, 46.

Kang, H., Lee, M. J., & Lee, J. K. (2012). Are you still with us? A study of the post-adoption determinants of sustained use of mobile banking services. Journal of Organizational Computing and Electronic Commerce, 22(2), 132–159.

Khan, A. G., Lima, R. P., & Mahmud, M. S. (2018). Understanding the service quality and customer satisfaction of mobile banking in Bangladesh: Using a structural equation model. Global Business Review, 22(1), 85–100. https://doi.org/10.1177/0972150918795551

Kim, B. (2010). An empirical investigation of mobile data service continuance: Incorporating the theory of planned behavior into the expectation-confirmation model. Expert Systems with Applications, 37(10), 7033–7039.

Kim, G., Shin, B., & Lee, H. G. (2009). Understanding dynamics between initial trust and usage intentions of mobile banking. Information Systems Journal, 19(3), 283–311.

Komulainen, H., & Saraniemi, S. (2019). Customer centricity in m-banking: A customer experience perspective. International Journal of Bank Marketing, 37(5), 1082–1102.

Lee, M. C. (2009). Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8, 130–141.

Lee, M. K. O., Cheung, C. M. K., & Chen, Z. H. (2007). Understanding user acceptance of multimedia messaging services: An empirical study. Journal of the American Society for Information Science and Technology, 58(13), 2066–2077.

Li, Y., & Wang, X. (2017). Online social networking sites continuance intention: A model comparison approach. Journal of Computer Information Systems, 57(2), 160–168.

Liu, Z., Min, Q., & Ji, S. (2009). An empirical study on mobile banking adoption: The role of trust. In 2009 Second International Symposium on Electronic Commerce and Security (Vol. 2, pp. 7–13). IEEE.

Looney, C. A., Jessup, L. M., & Valacich, J. S. (2004). Emerging business models for mobile brokerage services. Communications of the ACM, 46, 71–77.

Luarn, P., & Lin, H. H. (2005). Toward an understanding of the behavioral intention to use mobile banking. Computers in Human Behavior, 21(6), 873–891.

Makki, A. M., Ozturk, A. B., & Singh, D. (2016). Role of risk, self-efficacy, and innovativeness on behavioral intentions for mobile payment systems in the restaurant industry. Journal of Foodservice Business Research, 19(5), 454–473.

Marafon, D. L., Basso, K., Espartel, L. B., De Barcellos, M. D., & Rech, E. (2018). Perceived risk and intention to use internet banking: The effects of self-confidence and risk acceptance. International Journal of Bank Marketing, 36(2), 277–289.

McIver, J., & Carmines, E. G. (1981). Unidimensional scaling (No. 24). Sage.

Mladenovic, D., & Krajina, A. (2020). Knowledge sharing on social media: State of the art in 2018. Journal of Business Economics and Management, 21(1), 44–63. https://doi.org/10.3846/jbem.2019.11407

Mohammadi, H. (2015). A study of mobile banking usage in Iran. International Journal of Bank Marketing, 33(6), 733–759.

Mohammed, A. A., & Rozsa, Z. (2024). Consumers’ intentions to utilize smartphone diet applications: An integration of the privacy calculus model with self-efficacy, trust and experience. British Food Journal, 126(6), 2416–2437.

Moslehpour, M., Pham, V. K., Wong, W. K., & Bilgiçli, I. (2018). E-purchase intention of Taiwanese consumers: Sustainable mediation of perceived usefulness and perceived ease of use. Sustainability, 10, 234.

Mullan, J., Bradley, L., & Loane, S. (2017). Bank adoption of mobile banking: Stakeholder perspective. International Journal of Bank Marketing, 12(7), 1–32.

Muñoz-Leiva, F., Climent-Climent, S., & Liébana-Cabanillas, F. (2017). Determinantes de la intención de uso de las aplicaciones de banca para móviles: Una extensión del modelo TAM clásico. Spanish Journal of Marketing – ESIC, 21(1), 25–38. https://doi.org/10.1016/j.sjme.2016.12.001

Opaluch, R. E., & Tsao, Y. C. (1993). Ten ways to improve usability engineering: Designing user interfaces for ease of use. AT&T Technical Journal, 72, 75–88.

Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1985). A conceptual model of service quality and its implications for future research. Journal of Marketing, 49, 41–50.

Peterson, R. A., & Kim, Y. (2013). On the relationship between coefficient alpha and composite reliability. Journal of Applied Psychology, 98, 194–198.

Poromatikul, C., De Maeyer, P., Leelapanyalert, K., & Zaby, S. (2020). Drivers of continuance intention with mobile banking apps. International Journal of Bank Marketing, 38(1), 242–262.

Preacher, K. J., & Hayes, A. F. (2004). SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behavior Research Methods, Instruments, & Computers, 36, 717–731.

Püschel, J., Mazzon, A. J., & Hernandez, J. M. C. (2010). Mobile banking: Proposition of an integrated adoption intention framework. International Journal of Bank Marketing, 28(5), 389–409.

Qasim, H., & Abu-Shanab, E. (2016). Drivers of mobile payment acceptance: The impact of network externalities. Information Systems Frontiers, 18, 1021–1034.

Raudeliuniene, J., Davidaviciene, V., Tvaronaviciene, M., & Jonuska, L. (2018). Evaluation of advertising campaigns on social media networks. Sustainability, 10, 973. https://doi.org/10.3390/su10040973

Rogers, E. M. (1983). Diffusion of innovations (3rd ed.). Free Press.

Saadé, R., & Bahli, B. (2005). The impact of cognitive absorption on perceived usefulness and perceived ease of use in online learning. Information & Management, 42, 317–327.

Shaikh, A. A. (2013). Mobile banking adoption issues in Pakistan and challenges ahead. Journal of the Institute of Bankers Pakistan, 80(3), 12–15.

Shaikh, A. A., & Karjaluoto, H. (2015). Mobile banking adoption: A literature review. Telematics and Informatics, 32(1), 129–142. https://doi.org/10.1016/j.tele.2014.05.003

Shankar, A., Jebarajakirthy, C., & Ashaduzzaman, M. (2020). How do electronic word of mouth practices contribute to mobile banking adoption? Journal of Retailing and Consumer Services, 52, 101920.

Shin, Y. M., Lee, S. C., Shin, B., & Lee, H. G. (2010). Examining influencing factors of post-adoption usage of mobile internet. Information Systems Frontiers, 12(5), 595–606.

Singh, S., & Srivastava, R. K. (2018). Predicting the intention to use mobile banking in India. International Journal of Bank Marketing, 36(2), 357–378.

Tobbin, P. E. (2010). Modeling adoption of mobile money transfer: A consumer behaviour analysis. In 2nd international conference on mobile communication technology for development, Kampala, Uganda (pp. 1–8).

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478.

Wu, J. H., & Wang, S. C. (2005). What drives mobile commerce? An empirical evaluation of the revised technology acceptance model. Information & Management, 42(5), 719–729.

Yousafzai, S. Y., Foxall, G. R., & Pallister, J. G. (2010). Explaining internet banking behavior: Theory of reasoned action, theory of planned behavior, or technology acceptance model? Journal of Applied Social Psychology, 40(5), 1172–1202.

Zafiropoulos, K., Karavasilis, I., & Vrana, V. (2012). Assessing the adoption of e-government services by teachers in Greece. Future Internet, 4, 528–544.

Zhao, L., Lu, Y., Zhang, L., & Chau, P. Y. K. (2012). Assessing the effects of service quality and justice on customer satisfaction and continuance intention of mobile value-added services. Decision Support Systems, 52(3), 645–656.

Zhou, T. (2011). Understanding mobile internet continuance usage from the perspectives of UTAUT and flow. Information Development, 27(3), 207–218.

Zhou, T. (2015). Understanding user adoption of location-based services from a dual perspective of enablers and inhibitors. Information Systems Frontiers, 17(2), 413–422.

Appendix A

Informed Consent Form

Dear Respondent,

This questionnaire is purely for academic/research purposes. This questionnaire seeks to collect data on the topic: ‘Effects of Perceived Benefits and Risks on Continuance Intention of Using Mobile Banking Applications: User Satisfaction as Mediator’. For this research, we need some information from users of Mpay Delight+/YONO SBI.

The data collected would be used in aggregate, and no individual’s data would be named/quoted in the research. Please note that you are not required to disclose your identity while filling out this questionnaire. Therefore, you can be assured that your answers are completely confidential.

Your cooperation is highly important for the successful completion of the study. As such, it is requested to answer each statement included in the questionnaire correctly after due consideration.

Thanking you in advance.

Thank you for your precious time.